Characteristic |

exp(Beta) |

95% CI 1 |

|---|---|---|

| volatility_rank | ||

| volatility_ranklow | 0.45 | 0.42, 0.49 |

| volatility_rankmid | 0.63 | 0.58, 0.68 |

| mcap_rank | ||

| mcap_ranklow | 0.02 | 0.02, 0.02 |

| mcap_rankmid | 0.19 | 0.18, 0.21 |

| 1

CI = Credible Interval |

||

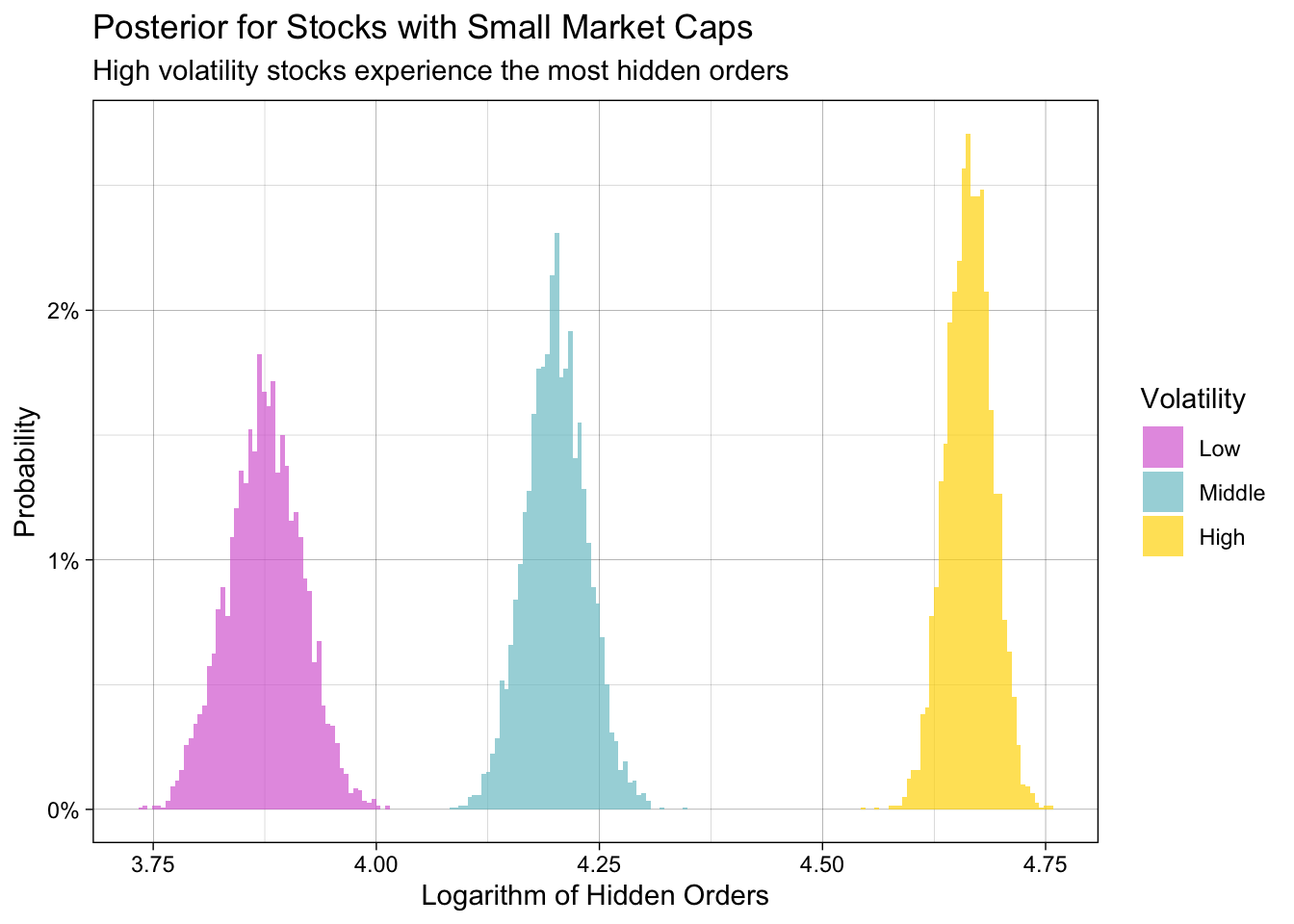

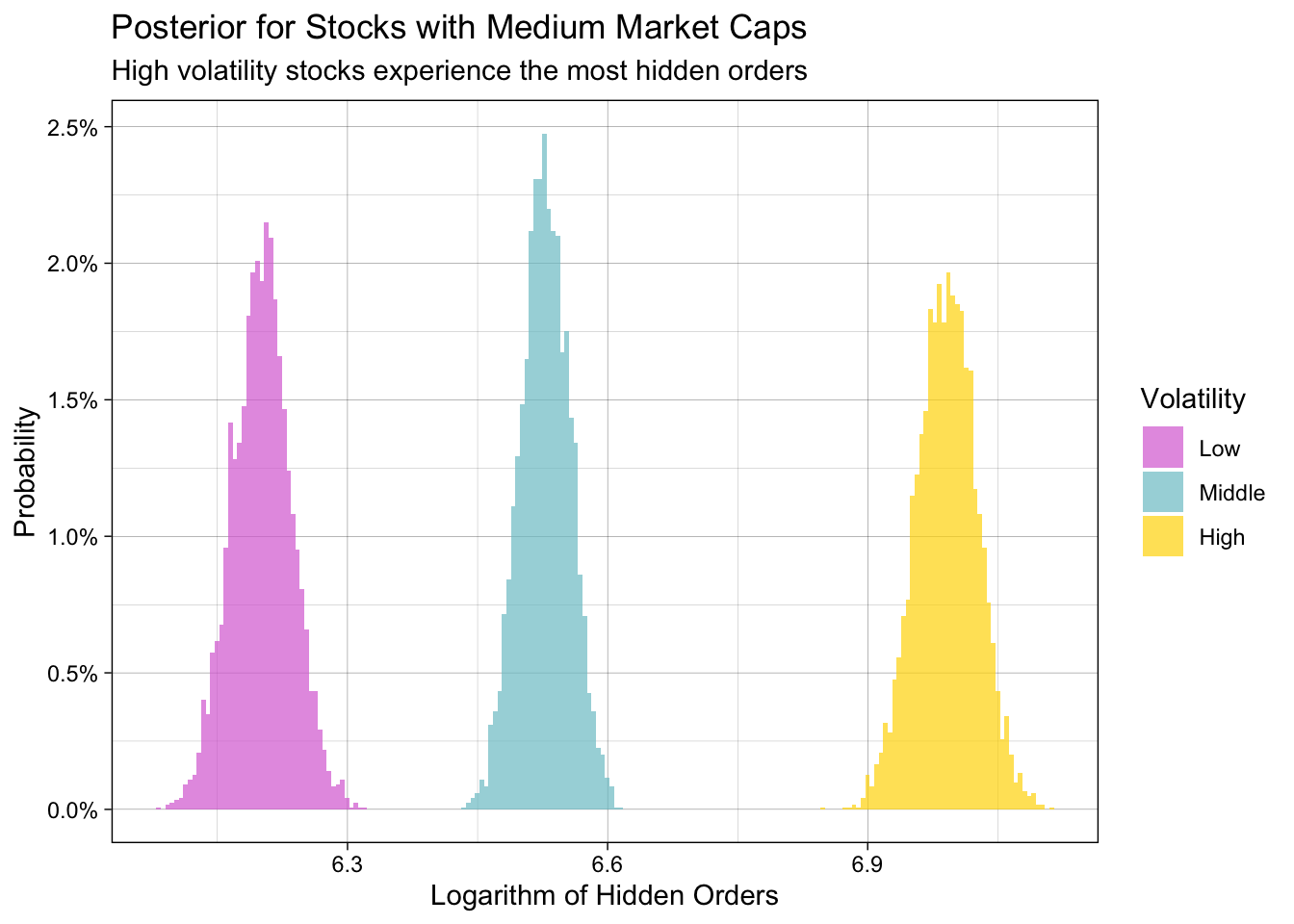

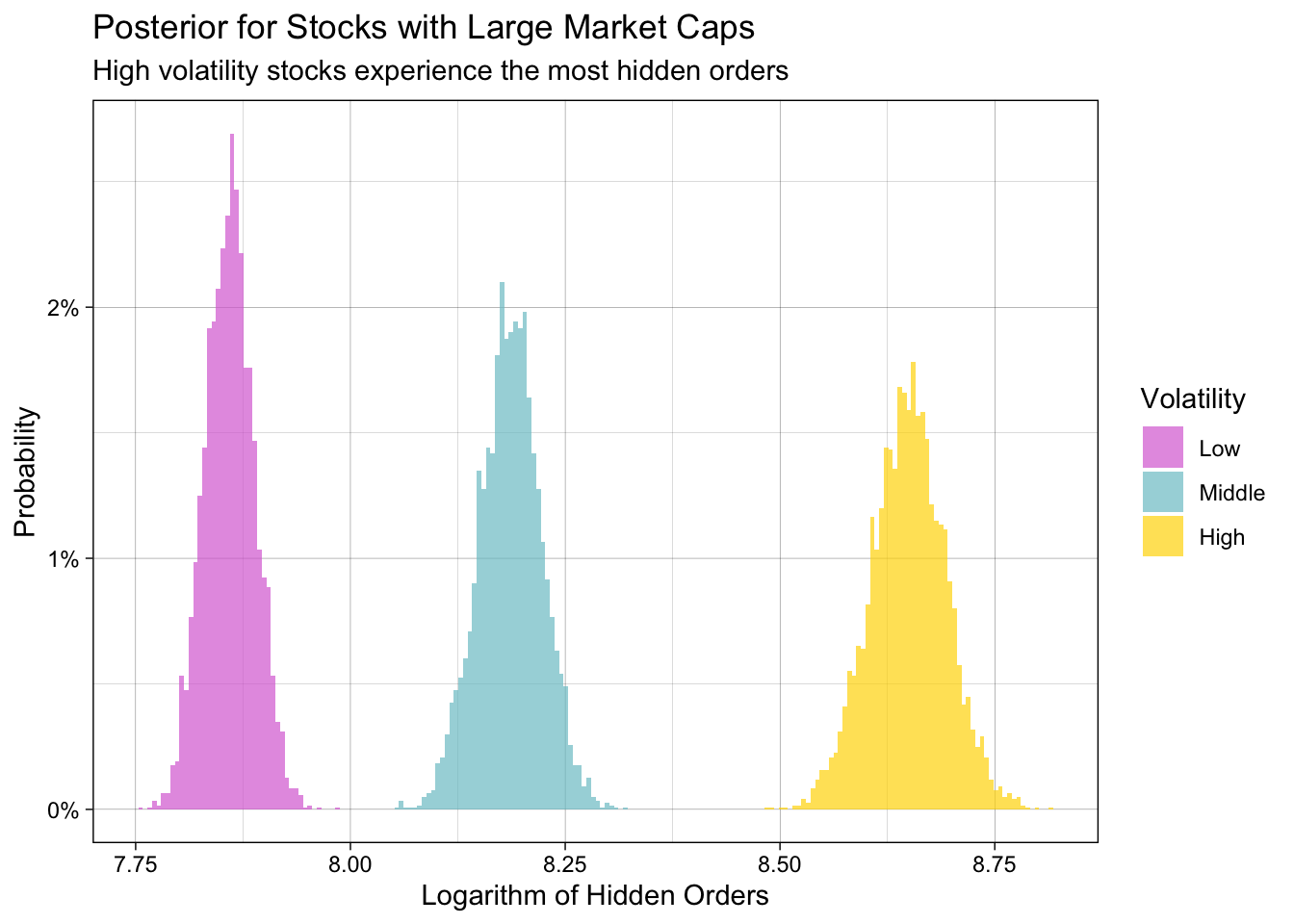

Model

Definition

\[\begin{aligned}y_{i} = \beta_1x_1 + \beta_2x_2+ \epsilon_{i}\\with\ y = log(hidden), x_1 = volatility\_rank, x_2 = mcap\_rank,\epsilon_{i}\sim (\mathcal{N}, \sigma^2)\end{aligned}\]

Parameters

Posteriors